Not Just Booking Engines

📅 5 February 2026 | 📂 Online Travel Agencies

The $253 Billion Personalization Gap Threatening Your Competitive Position

Enterprise OTAs are bleeding revenue through a hole in their platform architecture most executives don’t realize exists. While 71% of travelers expect personalized interactions from travel companies, and 76% express frustration when they don’t receive them, the majority of mid-market and enterprise OTAs still operate as transactional utilities—processing searches, displaying inventory, and completing bookings with minimal differentiation. The spontaneous travel decision market alone represents $253.3 billion in unmonetized opportunity, yet most platforms lack the infrastructure to capitalize on in-destination moments when travelers are most receptive to incremental purchases. Meanwhile, Booking.com has deployed AI-powered Smart Filters and Property Q&A features that instantly personalize search results using generative AI, and Expedia continues advancing its own AI personalization capabilities.

For CTOs at mid-market and enterprise OTAs, the question is no longer whether to evolve from utility to curator, but whether your technical architecture can make that transformation before competitors establish insurmountable advantages.

Why Technical Architecture Defines Competitive Position in 2026

The experience travel services market is projected to grow from $138 billion in 2024 to $372.93 billion by 2034, expanding at a 10.5% CAGR. This growth isn’t driven by increased transactional efficiency—it’s fueled by travelers’ willingness to pay premium prices for curated, personalized experiences that feel built specifically for them rather than assembled from generic inventory. Companies that master personalization generate approximately 40% more revenue than their peers, with personalized CTAs outperforming generic alternatives by 202%.

For OTA CTOs, this market shift creates a fundamental technical challenge: legacy platform architectures were designed to optimize search-and-book efficiency, not to deliver contextually relevant experience recommendations at scale. The technical debt accumulated through years of prioritizing booking conversion over post-booking engagement has created systems that excel at processing transactions but fail at relationship building. When travelers land in their destination, they typically abandon your platform because it offers no value beyond the initial booking—forcing them to TripAdvisor, Google, or competitor platforms that can surface relevant activities and experiences.

The competitive pressure is intensifying rapidly. Booking.com’s AI Trip Planner and Smart Filter capabilities demonstrate how platform leaders are leveraging generative AI to move beyond search functionality into proactive trip curation. These aren’t incremental feature additions—they represent architectural pivots that position platforms as intelligent travel advisors rather than digital storefronts. For CTOs at mid-market OTAs, the strategic question becomes: how do you close this capability gap without multi-year development timelines that allow competitors to establish market dominance?

The Technical Reality: Why Building In-House Fails

Most OTA CTOs underestimate the technical complexity required to transform booking platforms into experience curators. The challenge isn’t simply adding an “activities” tab or integrating a third-party marketplace—it’s building comprehensive infrastructure capable of delivering personalized, contextually relevant recommendations at scale across 550+ global destinations.

The technical requirements break into several layers, each presenting significant development and operational challenges:

Experience Intelligence Layer: Unlike hotel or flight inventory with standardized attributes (price, location, dates), experiences vary dramatically in seasonality, weather dependency, physical requirements, and cultural context. Building a recommendation engine requires experience taxonomy systems, real-time availability integration, quality scoring algorithms, and contextual relevance models that understand when a wine tour makes sense versus an adventure activity. Most OTAs lack the destination expertise and content infrastructure to build this intelligence internally.

Personalization Engine: Effective curation demands understanding individual traveler preferences, trip context, party composition, booking history, and behavioral signals—then matching those attributes against experience characteristics in real-time. This requires customer data platforms, machine learning models, A/B testing infrastructure, and personalization APIs that most mid-market OTAs don’t possess. Building these systems requires 12-18 months of development time and specialized data science teams that face 40-60% annual attrition rates in competitive talent markets.

Supplier Integration Framework: Experience providers operate on fragmented booking systems with inconsistent APIs, availability protocols, and pricing structures. Aggregating meaningful inventory requires individual supplier integrations, ongoing relationship management, quality assurance processes, and dispute resolution systems. OTAs that attempt this in-house typically launch with 50-100 experiences in 3-5 destinations after 9-12 months of development, creating insufficient selection to drive meaningful engagement or revenue.

The opportunity cost of these development timelines is substantial. A CTO who commits 18 months to building experience infrastructure delays market entry while competitors establish customer habits and supplier relationships. Meanwhile, the core booking platform requires ongoing investment in performance optimization, security updates, and feature parity with evolving market standards. Resource allocation becomes a zero-sum game where pursuing curation capabilities starves essential platform maintenance.

The Integration Architecture That Enables Speed

The alternative approach—treating experience curation as a specialized utility rather than core platform functionality—enables dramatically faster time-to-market while preserving technical flexibility. Modern API-first architectures allow OTAs to embed sophisticated recommendation and booking capabilities without rebuilding foundational systems.

The key architectural principle is separation of concerns: the OTA platform maintains authority over customer identity, booking flow orchestration, and transaction processing, while specialized experience curation systems handle recommendation intelligence, content management, and supplier coordination. This enables OTAs to leverage external expertise in destination intelligence and experience taxonomy while maintaining brand control and customer ownership.

Successful implementations follow several technical patterns:

Embedded API Integration: Rather than redirecting users to third-party marketplaces, leading OTAs embed recommendation and booking widgets directly into post-booking confirmation flows, pre-trip emails, and mobile app experiences. This maintains consistent brand experience while leveraging specialized recommendation engines. API response times under 200ms ensure these embedded experiences feel native to the platform rather than bolted-on features.

Progressive Data Enrichment: Instead of requiring complete customer profile migration, effective integrations start with minimal context (destination, travel dates, party composition) and progressively incorporate preference signals as users interact with recommendations. This reduces integration complexity while building toward sophisticated personalization over time.

Unified Commerce Layer: The most seamless implementations treat experience bookings as first-class transactions within the OTA’s existing commerce infrastructure. Customers see experience purchases in their trip itinerary alongside flights and hotels, receive consolidated confirmations, and access unified support—all while backend systems handle supplier coordination and fulfillment orchestration.

This architectural approach enables 4-6 week integration timelines rather than 12-18 month build cycles, allowing CTOs to test market response and iterate based on actual customer behavior rather than projected requirements.

Strategic Evaluation: Build, Buy, or Partner

CTOs evaluating platform-versus-utility positioning face three architectural paths, each with distinct technical and strategic implications:

Build In-House: This approach offers maximum control over feature roadmap, customer data, and supplier relationships but requires substantial upfront investment and ongoing operational overhead. In-house builds make strategic sense when experience curation represents a core differentiator that justifies multi-year development commitment and dedicated team allocation. However, most mid-market OTAs lack the scale to justify the $2-3 million development investment plus ongoing operational costs for supplier management, content curation, and customer support.

Acquire Marketplace Technology: Some OTAs pursue acquisition of smaller experience platforms to gain technology and supplier relationships. This accelerates capability development but introduces integration complexity, cultural alignment challenges, and ongoing maintenance of acquired systems. Acquisition economics require sufficient scale to amortize purchase costs across substantial booking volume—typically viable only for enterprise OTAs processing 1M+ annual transactions.

API Partnership Model: This path prioritizes speed-to-market and operational efficiency over maximum control. OTAs integrate specialized experience platforms via API, leveraging external investment in recommendation engines, supplier relationships, and operational infrastructure. The tradeoff is dependency on partner roadmap and potential revenue sharing, balanced against immediate market entry and minimal technical risk. For most mid-market OTAs, this represents the optimal path to competitive positioning while preserving technical resources for core platform differentiation.

The evaluation framework should prioritize:

Speed to Market: How quickly can each approach generate customer-facing capability and revenue impact?

Total Cost of Ownership: What is the 3-year fully loaded cost including development, operations, and opportunity cost?

Technical Flexibility: Does the approach preserve architectural optionality or create lock-in?

Quality at Scale: Can the solution deliver sophisticated personalization across meaningful destination coverage?

Most CTOs find that partnership models offer superior risk-adjusted returns, enabling experience curation capabilities in weeks rather than quarters while maintaining focus on core platform innovation

Implementation Roadmap: From Utility to Curator

For CTOs ready to advance platform positioning, successful transformations follow a phased approach that balances speed with technical rigor:

Phase 1: Post-Booking Activation (Weeks 1-6): Begin with post-booking touchpoints where customer context is richest and risk is lowest. Integrate personalized experience recommendations into booking confirmation emails and post-purchase pages. This validates technical integration, tests customer engagement, and generates early revenue without disrupting core booking flows. Success metrics focus on recommendation click-through rates (target: 8-12%) and conversion to booking (target: 3-5%).

Phase 2: Pre-Trip Engagement (Weeks 6-12): Expand recommendations into pre-trip email campaigns and mobile app experiences. This capitalizes on trip anticipation when travelers actively research destinations. Progressive profiling captures preference signals that inform future recommendations. Success metrics expand to include average order value (target: $150-250 per experience booking) and attachment rate (target: 15-25% of hotel bookings generate experience purchase).

Phase 3: In-Destination Activation (Weeks 12-20): Deploy mobile push notifications and contextual in-app recommendations based on real-time location and itinerary status. This captures spontaneous decision-making moments when travelers are most receptive to immediate experiences. Success metrics track incremental revenue per traveler and in-destination booking conversion rates.

Phase 4: Pre-Booking Integration (Months 6-9): Introduce experience recommendations during initial trip planning and hotel search processes. This positions the platform as comprehensive trip planner rather than accommodation specialist. Success metrics measure impact on overall booking value and platform engagement.

Throughout implementation, technical teams should prioritize API performance, error handling, and fallback strategies that ensure recommendation failures never impact core booking functionality. Comprehensive logging and analytics infrastructure enables rapid iteration based on customer behavior patterns.

Security and compliance considerations require careful attention, particularly regarding customer data sharing with integration partners, PCI compliance for experience payments, and GDPR compliance for EU customers. Technical due diligence should verify partner security certifications, data processing agreements, and liability frameworks before production deployment.

From Architecture Decision to Market Position

The strategic question facing OTA CTOs isn’t whether to evolve platform capabilities—market dynamics make that inevitable. The critical decision is whether to build curation infrastructure in-house or leverage specialized partners that enable immediate market entry.

CTOs who recognize experience curation as specialized utility rather than core platform functionality gain decisive advantages:

- 4-6 week integration timelines versus 12-18 month build cycles enable immediate competitive response

33% average revenue increases per customer through incremental experience bookings that complement accommodation revenue - 300,000+ curated experiences across 550+ destinations that no mid-market OTA could economically build internally

- 51% average redemption rates demonstrating genuine customer engagement rather than ignored recommendations

- The platform-versus-utility decision ultimately determines whether OTAs can transform from commodity booking engines into differentiated travel brands that own customer relationships beyond initial transactions.

For CTOs evaluating platform transformation:

- Audit current technical architecture: Assess API readiness, customer data accessibility, and commerce infrastructure flexibility

- Model revenue impact: Calculate incremental revenue potential using 15-25% attachment rates and $150-250 average order values against current booking volume

- Request technical architecture review: Evaluate integration approaches, security protocols, and performance implications with potential partners

- Access OpenAPI specifications: Review detailed integration requirements to validate technical feasibility and development timelines

The travel industry’s evolution from transactional utility to experiential curator represents a permanent market shift. CTOs who act decisively position their platforms for sustainable competitive advantage while those who delay cede market position to more agile competitors. The technical architecture decisions you make today determine whether your OTA remains relevant in tomorrow’s experience-driven travel landscape.

Ready to explore technical architecture options? We’d love to hear from you.

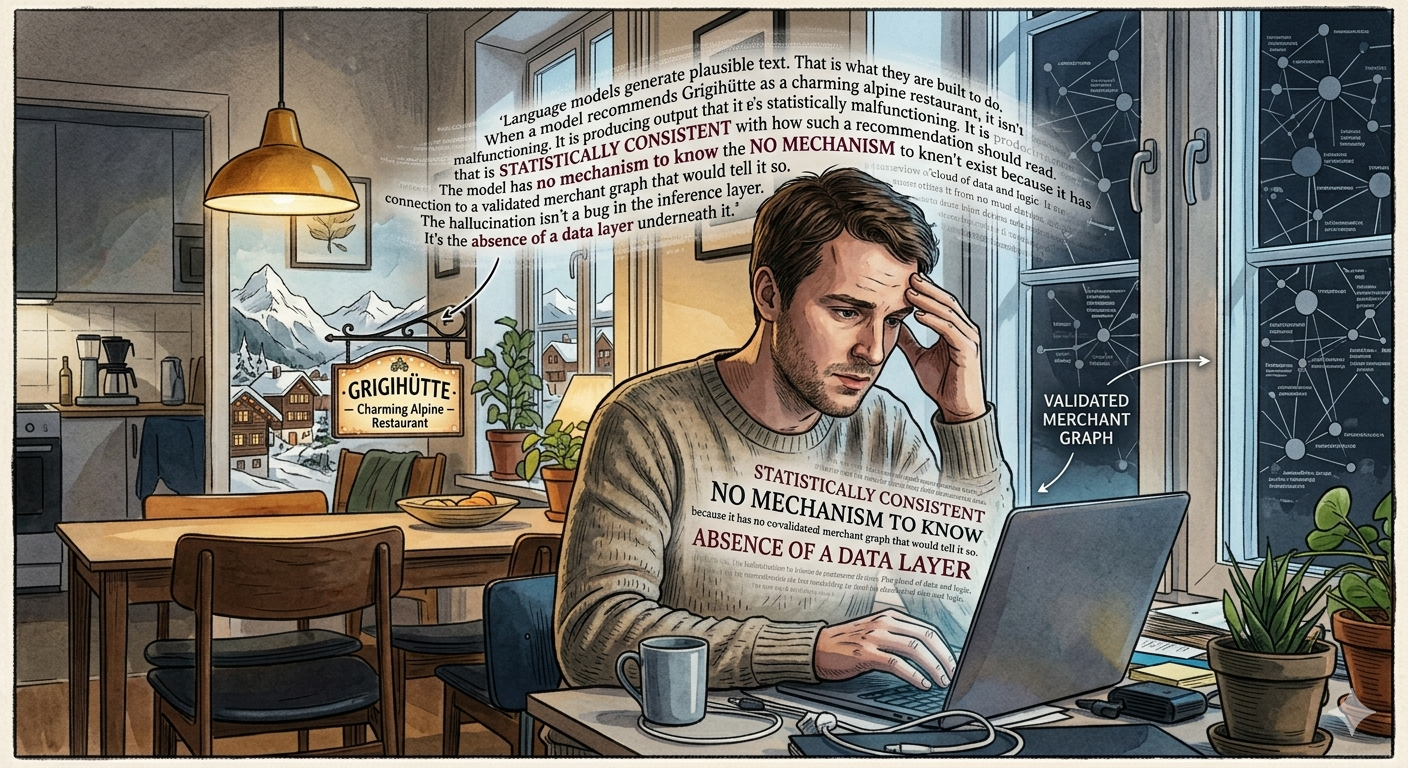

Your Trip Planner Is Lying. Here’s Why.

A credible study just handed your AI roadmap a liability. In testing published by Forbes and InsureMyTrip, AI-powered travel planning tools recommended restaurants, attractions, and experiences that simply do not exist. Not outdated listings. Not temporary closures. Fabrications, complete with…

You Win the Booking. You Lose the Journey.

Forty-four percent of in-destination activities are booked outside the platform that originated the trip. Not because travelers are disloyal. Because the platform gave them no reason to stay. The Funnel You Built Isn’t Broken — It’s Just Incomplete The OTA…

The Platform Era in Travel:

Why Connectivity Determines Competitive Advantage

Enterprise OTAs and DMCs are losing between $8-15M annually to a problem hiding in plain sight: 44% of spontaneous in-destination bookings happen outside their platforms. While your systems capture the initial flight and hotel reservation, travelers are booking experiences through…