📅 27 January 2026 | 📂 In-Destination Revenue, Online Travel Agencies

Competitive Intelligence for Mid-Market OTAs

Booking.com’s AI Trip Planner represents more than a feature launch; it’s a strategic repositioning from transactional booking utility to inspirational travel curator that mid-market OTAs must decode and counter.

When 71% of travelers expect AI-driven personalization and the $253.3B experience economy grows at 8.2% annually, understanding Booking.com’s playbook becomes existential for competitors struggling to capture 44% of spontaneous in-destination bookings. The question isn’t whether to respond, but how to execute a competitive strategy without Booking.com’s R&D budget or 18-month development timelines.

Booking.com launched their AI Trip Planner in beta to US travelers in June 2023, expanding globally throughout 2024-2025 to UK, Australia, New Zealand, Singapore, and European markets with localized language support. By October 2025, they’d evolved from standalone trip planning tool to integrated AI companion with Smart Messenger and Auto-Reply features managing real-time disruptions like flight cancellations. This phased approach demonstrates their core strategy: iterative deployment allowing continuous learning while maintaining brand trust and operational stability across millions of daily users.

Booking.com’s Technical Architecture: Speed Through Integration

Booking.com’s technical strategy reveals the competitive advantage mid-market OTAs often overlook: strategic integration over custom development. Their team built the AI Trip Planner in approximately 10 weeks by combining existing machine learning infrastructure—which already recommends destinations and accommodations to millions daily, with OpenAI’s ChatGPT API for conversational capabilities. This wasn’t a ground-up AI build; it was intelligent orchestration of proven technologies with proprietary travel data.

The architecture merges structured data (pricing, availability, cancellation policies, property ratings) with unstructured data (user reviews, natural language descriptions, contextual queries) to generate curated suggestions. Mid-market OTAs possess similar data assets—booking history, customer preferences, destination inventory, but frequently lack the AI layer activating this information at scale. Booking.com’s breakthrough demonstrates that competitive AI personalization doesn’t require rebuilding your entire tech stack; it requires the right integration strategy.

Their deployment model prioritized market validation over perfection.

US beta in June 2023 provided real-world feedback before expanding to English-speaking markets, then European destinations with full localization. By 2025, Booking.com’s AI Trip Planner evolved beyond destination discovery to proactive trip management, Smart Filter for natural language property search, Property Q&A answering specific questions from listing data, and Review Summaries distilling insights without manual browsing. This iterative enhancement strategy compounds competitive advantage: each feature builds on proven infrastructure while competitors remain stuck in 18-month development cycles.

The Strategic Intent: Owning the Entire Travel Journey

From Booking Engine to Travel Companion

Booking.com’s AI strategy fundamentally repositions their value proposition from accommodation marketplace to end-to-end travel experience curator. The AI Trip Planner addresses every planning stage: destination exploration (“romantic beach destinations in Caribbean”), itinerary creation for specific cities, accommodation recommendations matching preferences, and even in-destination activity suggestions while travelers are on trips. This comprehensive approach captures wallet share across the entire travel journey—not just the accommodation booking moment.

The competitive implications are profound. When travelers use Booking.com’s AI for destination inspiration, itinerary planning, and activity discovery, they’re less likely to complete experience bookings through GetYourGuide direct, Viator, or mid-market OTA competitors. Booking.com transforms from transaction facilitator to trusted travel advisor, a relationship commanding significantly higher customer lifetime value and repeat booking rates. Mid-market OTAs still competing on accommodation price comparisons face margin compression while Booking.com monetizes higher-margin ancillaries.

The data flywheel effect compounds this advantage. Each traveler interaction with the AI Trip Planner, questions asked, destinations browsed, properties saved, activities booked, feeds machine learning models improving future recommendations. Mid-market OTAs starting AI initiatives today face a growing data and algorithm sophistication gap that widens with each passing quarter.

Capturing the Experience Economy

Booking.com’s integration of activities and experiences directly into AI-generated itineraries targets the fastest-growing, highest-margin segment of travel spending. The 41% of travelers interested in AI-curated itineraries aren’t just seeking accommodation recommendations; they want complete trip solutions including tours, attractions, dining, and transportation. Booking.com’s strategy positions them to capture 20-30% commission rates on experiences versus 10-15% on hotel bookings.

The AI Trip Planner’s conversational interface lowers friction for discovery and booking. Instead of navigating complex category taxonomies or conducting multiple searches, travelers describe their preferences in natural language (“family-friendly activities in Barcelona”) and receive personalized recommendations with deep-links to booking pages. This seamless integration drives higher conversion rates than separate experience marketplaces requiring additional navigation and decision-making.

Booking.com’s timing aligns with demographic shifts favoring experience-driven travel. Gen Z and Millennials (representing 40% of the travel market by 2026) prioritize authentic experiences over traditional points-based loyalty programs. AI-powered personalization matching individual preferences to local experiences creates differentiation that price competition cannot replicate.

Competitive Response Strategies for Mid-Market OTAs

The Build vs. Buy Decision Framework

Mid-market OTAs evaluating competitive responses to Booking.com’s AI Trip Planner face a critical fork: build proprietary AI personalization or integrate proven platforms enabling rapid deployment. Building in-house requires 18-24 months and $2-5M investment covering POI data curation (4M+ points of interest across 550+ destinations), machine learning infrastructure, recommendation algorithms, supplier API integrations (300K+ bookable experiences), mobile SDKs, and multilingual support. Engineering teams estimate 10-15 full-time engineers dedicated to development, then 3-5 FTEs for ongoing maintenance.

The opportunity cost multiplies the direct expense. Each quarter of development delay represents $1-3M in foregone ancillary revenue as Booking.com and Expedia capture spontaneous bookings your platform cannot facilitate. If Booking.com launched their AI Trip Planner in 10 weeks by integrating OpenAI capabilities with existing ML infrastructure, mid-market players spending 18 months on custom builds are solving the wrong strategic problem.

Legacy system integration presents the hidden complexity CTOs underestimate. Mid-market OTAs report that 10-15 year old booking engines lack modern API interfaces, requiring complex middleware extending timelines and introducing failure points. Technical debt currently consuming 30-40% of engineering capacity means diverting developers to AI projects delays core platform improvements, security updates, and customer experience enhancements.

API-First Integration as Competitive Acceleration

The strategic alternative prioritizes speed to market through API-first partnerships with specialized AI personalization vendors. This approach leverages vendors’ scale advantages, 4M POIs maintained across 550 destinations, 300K pre-integrated bookable experiences, proven ML algorithms serving millions of travelers, and enterprise-grade security infrastructure. Integration timelines compress from 18 months to 4-6 weeks through multiple deployment paths: white-label web apps embeddable via iframe (2 weeks), RESTful API integration with mobile SDKs (4-6 weeks), or custom deep integration optimizing entire booking flows (6-8 weeks).

The economic model shifts from CapEx to variable OpEx aligned with performance. Commission-share pricing (15-25% of net revenue on AI-driven bookings) means zero cost if recommendations don’t convert, eliminating upfront investment risk while aligning vendor incentives with OTA outcomes. For mid-market OTAs with 100K-500K annual travelers, this translates to $250K-750K annual cost versus $2-5M build investment, with revenue generation starting in Q1 2026 instead of Q3 2027.

White-label deployment preserves brand control and customer relationships, a critical concern for OTAs protective of direct customer connections. Fully branded UIUX maintains the OTA’s presentation throughout discovery, recommendation, and booking, with zero vendor visibility to travelers. All bookings attribute to the OTA for revenue recognition, customer data capture, and lifecycle marketing.

Differentiation Through Hybrid Marketplace Strategy

Mid-market OTAs cannot match Booking.com’s global scale but can differentiate through localized, curated experiences leveraging regional expertise. Hybrid marketplace approaches blend proprietary inventory (exclusive partnerships with local DMCs, unique experiences, preferred suppliers) with comprehensive third-party aggregators (GetYourGuide, Viator, Musement) to offer both differentiated content and competitive breadth. Configurable business rules prioritize high-margin exclusive experiences in recommendations while maintaining comprehensive coverage for customer choice.

This strategy addresses supplier relationship concerns preventing many OTAs from deploying AI personalization. Rather than replacing existing GetYourGuide or Viator partnerships, AI platforms can feature current suppliers first in recommendations while filling inventory gaps in secondary destinations or emerging categories. The AI personalization layer increases conversion on existing supplier catalogs from 5-8% baseline to 15-20%, generating more volume through current partnerships and justifying improved commission terms.

Regional specialization creates defensible competitive moats Booking.com struggles to replicate. A Caribbean-focused OTA integrating 600 local merchants with personalized recommendations based on island-specific expertise offers authenticity and discovery global platforms cannot match. European OTAs with deep destination knowledge in secondary cities (Lyon, Porto, Krakow) can curate experiences showcasing local culture beyond mass tourism attractions dominating Booking.com’s inventory.

Implementation Without Disruption

Phased Rollout Mitigating Risk

Mid-market OTAs burned by vendor promises demand proof before full commitment. Pilot programs with clear attribution methodology provide statistical validation of incremental revenue. A/B testing deploys AI recommendations to 10-20% of traffic while control groups receive current generic suggestions, isolating the personalization impact from seasonal variations, marketing campaigns, and destination mix changes.

Success metrics define go/no-go decisions: 15-20% attach rates on AI recommendations (versus 5-8% baseline), $180-220 average order value on experience bookings (versus $120-150 baseline), 40-60% engagement rates on personalized itineraries (versus 10-15% on generic emails), and 4.5+ star ratings validating recommendation quality. Pilots typically run 8-12 weeks providing sufficient data for statistical significance while enabling full production launch before peak summer travel season.

Kill-switch capability protects brand and customer experience during pilots. If AI recommendations generate customer complaints, lower NPS scores, or underperform baseline conversion rates, OTAs can disable the feature instantly and revert to previous experiences. This de-risks deployment compared to custom builds lacking easy rollback options.

Technical Architecture for Speed

Integration velocity depends on architectural approach and existing technical debt. Dedicated solutions architects managing end-to-end integration reduce internal burden to one product manager and one developer working part-time for 4-6 weeks—the rest of the engineering team continues core platform work uninterrupted.

Phased deployment through sandbox (week 1), staging (weeks 2-3), pilot production at 10% traffic (week 4), and full rollout (week 6) provides validation gates at each stage.

The integration must not disrupt core booking engines, payment systems, or customer databases. Microservice architecture treating AI personalization as standalone service minimizes risk to production systems. RESTful APIs with comprehensive OpenAPI documentation enable faster development than legacy SOAP interfaces common in older booking platforms. Mobile SDKs for iOS, Android, and web allow consistent experiences across channels without separate development efforts.

Security and compliance requirements cannot be compromised for speed. AWS GDPR-compliant infrastructure, PCI/FedRamp logging, 7-day data retention policies, and zero PII collection by vendor systems address data privacy concerns while maintaining rapid deployment. SOC 2 Type II certification and penetration testing reports satisfy CISOs evaluating third-party integration risk.

Strategic Takeaways

Mid-market OTAs cannot ignore Booking.com’s AI Trip Planner strategy, it fundamentally redefines competitive dynamics in online travel:

- Speed trumps perfection: Booking.com launched AI capabilities in 10 weeks by integrating existing technologies rather than building everything custom. Mid-market players spending 18 months on in-house development forfeit $5-15M in cumulative foregone revenue.

- Experience integration drives differentiation: AI Trip Planners capturing destination discovery, itinerary planning, and activity bookings create higher customer lifetime value than accommodation-only platforms. The 44% of spontaneous in-destination bookings represents $10-25M annual opportunity for mid-market OTAs.

- API-first architecture enables competitive parity: Integration strategies compressed to 4-6 weeks allow mid-market OTAs to deploy enterprise-grade AI personalization without proportional R&D investment. White-label deployment preserves brand control while leveraging specialized vendors’ scale advantages.

- Pilot validation de-risks decisions: A/B testing with 10-20% of traffic provides statistical proof of incremental revenue before full deployment. Performance-based pricing (commission-share on bookings) eliminates upfront capital risk.

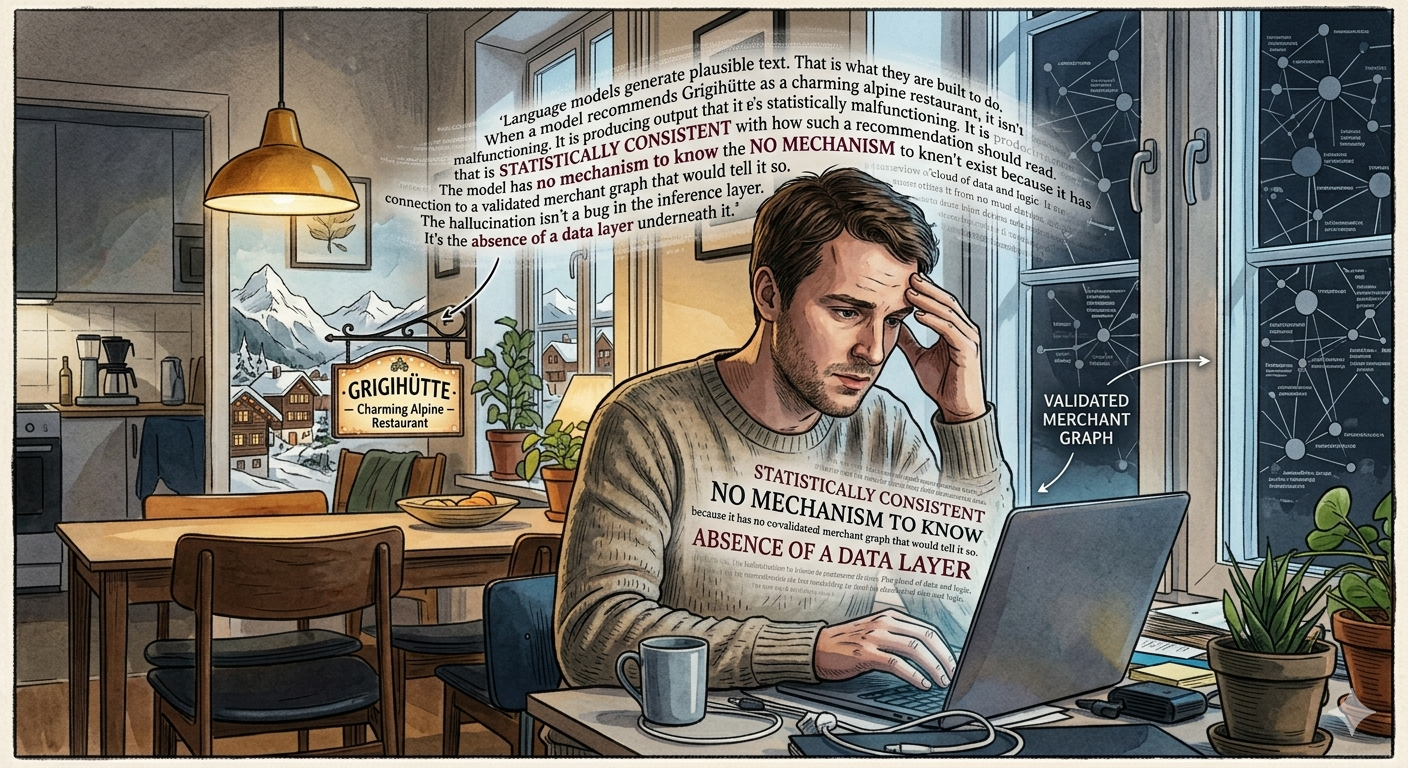

Your Trip Planner Is Lying. Here’s Why.

A credible study just handed your AI roadmap a liability. In testing published by Forbes and InsureMyTrip, AI-powered travel planning tools recommended restaurants, attractions, and experiences that simply do not exist. Not outdated listings. Not temporary closures. Fabrications, complete with…

You Win the Booking. You Lose the Journey.

Forty-four percent of in-destination activities are booked outside the platform that originated the trip. Not because travelers are disloyal. Because the platform gave them no reason to stay. The Funnel You Built Isn’t Broken — It’s Just Incomplete The OTA…

The Platform Era in Travel:

Why Connectivity Determines Competitive Advantage

Enterprise OTAs and DMCs are losing between $8-15M annually to a problem hiding in plain sight: 44% of spontaneous in-destination bookings happen outside their platforms. While your systems capture the initial flight and hotel reservation, travelers are booking experiences through…